In Summary

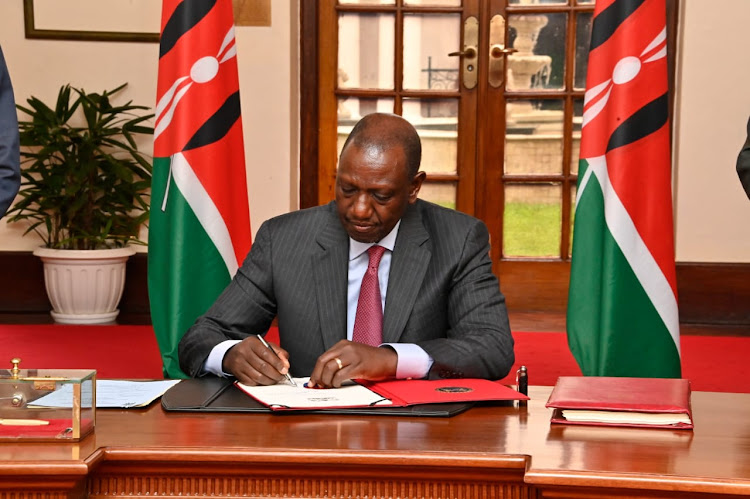

- The Insurance Act (Cap.487) has been amended to provide for offences and penalties relating to the management of insurance companies.

- It will ensure that insurance company managers are more accountable for losses arising from their companies.

President William Ruto when he assented into law the Insurance amendment bill, 2023.

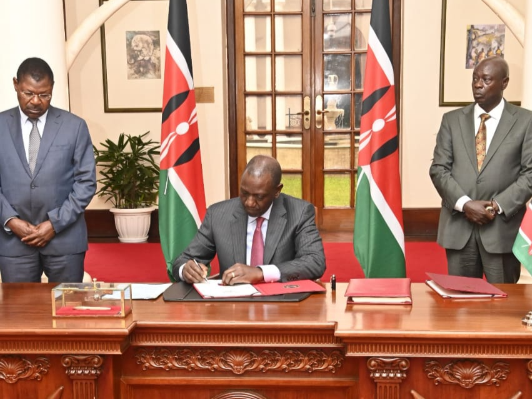

National Assembly speaker Moses Wetangula (left) and Deputy President Rigathi Gachagua look on as President William Ruto sign into the law the supplementary appropriation Bill, 2023 at Statehouse on November 23, 2023.