The government recently launched the National Infrastructure Fund and

established the legal framework to implement it.

President William Ruto

assented to the law in early March, paving the way for the constitution of its board

of management and other governance structures. Henceforth, this will be the

main avenue for raising resources for national development projects.

Kenya, like other developing countries, has historically relied on

external assistance from the First World to fund major development projects. At

the initial stages, soon after Independence, the former colonial masters were

the first port of call for emerging nations.

In their effort to establish and

maintain strategic interests, more developed countries offered development

assistance with heavy conditionalities.

These loans often came through the

Bretton Woods institutions of the World Bank and the IMF. The two institutions were

controlled by the United States and her allies in the NATO and pushed their

Cold War agenda.

Then along the way came Japan and most recently China entered the scene

with a bang. The Chinese took advantage of the end of the Cold War to entice

the Global South with support in trade development.

Initially, this appeared

balanced and lucrative but it has proved to be equally expensive as any other

commercial loan. Kenya’s ambitious development plan under the Beta policy was at peril if no such innovative

initiative was designed.

Massive infrastructure projects such as the Rironi-Mau Summit Road, the Naivasha-Kisumu Standard Gauge Railway and the dualling of Mombasa and Machakos

roads would all meet a dead end.

The affordable housing project requires a

significant supply of electricity and water. These require injection of huge

capital that the government can only obtain at exorbitant cost from the

international financial markets.

The National Infrastructure Fund (NIF) in Kenya, signed into law by President Ruto in March is a strategic

vehicle aimed at mobilising Sh5 trillion over the next decade to finance major

projects — such as roads, dams and energy — through private sector investment

rather than increased sovereign debt.

The fund will be capitalised through

proceeds from the privatisation of state assets, starting with Sh106 billion

from the Kenya Pipeline Company IPO.

The main objective of this state apparatus

is to shift national development funding from a debt-driven model to an

investment-led model for infrastructure, focusing on commercially viable

projects to reduce the debt burden.

It targets initial sources for resourcing from proceeds of privatisation

(e.g., KPC, potential Safaricom stake sales), public-private partnerships and institutional capital (pension funds, etc).

From its blueprint, the

initiative aims to undertake mega projects, including 10,000MW of clean energy,

50 mega dams, 2,500km of dual carriageways, 28,000km of roads, SGR expansion to

Malaba-Kisumu and JKIA modernisation.

The statutory framework has ringfenced its governance structure as an

independent corporate entity with a board of directors to ensure professional management,

overseen by a governing council. It has

inbuilt fiduciary deterrents that include strict penalties for misappropriation

and oversight by the Office of the Auditor-General.

The NIF is designed to

operate independently, with a five-year investment policy to protect project

funding from political cycles with the broad objective to lower transportation

and logistics costs, stimulate job creation, and accelerate industrial growth.

Progressively, national external debt has been growing, diminishing the opportunity for transformative development projects. On December 12, 1963, Kenya’s external relations were defined by a swift

transition from British colonial rule to a sovereign state within the

Commonwealth, initially as a constitutional monarchy.

The nation adopted a

pro-Western, anti-communist foreign policy while navigating Cold War tensions

and establishing its diplomatic footprint in major global capitals.

The

founding administration inherited a relatively modest debt burden of about

Sh1.72 billion (about $240 million at the time). This initial debt was mostly

related to development projects and was considered manageable as the economy

was growing by 6.5 per cent annually during the first decade, maintaining a

stable external balance.

However, a decade later Kenya’s total external public

debt was about $845 million. This marked a significant 45.4 per cent increase

from $581 million in 1972, driven by the first oil crisis and increased

borrowing. Despite this, the debt-servicing ratio remained low, although the

era marked the beginning of heavier external borrowing.

Kenya’s total external debt in 1998 was about $6.82 billion. During this

period, the country was experiencing a challenging economic environment, with

the external debt-to-GNI ratio hovering around 49 per cent.

The government was

also managing significant debt arrears, including a notable $70.95 million

rescheduling agreement with the Banque Nationale de Paris. In 2003, Kenya’s

total external debt was about $3.6 billion in Net Present Value terms.

The

total external debt stock for that year was reported to be around $6.72

billion. During this period, the country was experiencing a relatively low,

stabilising external debt, with a record low of Sh361.731 billion achieved in

May.

As of early this year, Kenya’s external

debt stands at about Sh5.46 trillion to Sh5.48 trillion ($41-43 billion),

contributing to a total public debt of more than Sh12 trillion.

While the

external debt has stabilised due to a stronger shilling, it represents a

high-risk factor, with debt servicing consuming more than 71 per cent of

government revenue.

It is therefore clear that the national external debt has steadily been

rising since Independence. The financing has become expensive to taxpayers and

yet the country requires intense investment in transformative development

projects.

The answer lies squarely in innovative internal resource

mobilisation. NIF has responded appropriately to this challenge. It is

commendable that the government has made considerable strides in meeting its

debt obligations.

However, the demands for fresh funds to finance development projects is

a heavy burden on the shoulders of the current coalition of the broad-based

government. The NIF as crafted is a game changer in national reconstruction and

renaissance. It speaks directly to the heart and spirit of the pan-African dream.

Envisaged by the region’s

founding fathers as emancipation from the shackles of neocolonialism, the

ideology foresees a united continent with sufficient resources for consumption

and development.

The African continent is arguably the richest in terms of

natural resources, including rare minerals used by giant tech companies on the

cutting-edge digital economy.

It is these resources that led to its

colonisation and later its puppet status in the neocolonial chess game. Control

of destiny can only be meaningfully achieved through self-reliance in

supporting society’s consumption and development needs.

Economic self-reliance logically assures of true political independence.

This was the passionate dream of the Independence leaders. Pan-Africanist ideas

first began to circulate in the mid-19th century in the United States, led by

Africans from the Western Hemisphere.

The most important early Pan-Africanists

were Martin Delany and Alexander Crummel, both African Americans, and Edward

Blyden, a West Indian.

The first African-born Prime Minister of Ghana, Kwame

Nkrumah, was a prominent Pan-African organiser whose radical vision and bold

leadership helped lead Ghana to independence in 1957.

Through the OAU and

currently the AU, Pan-Africanism has been at the core of Africa’s economic and

political freedom. Agenda 2063 is the continent’s blueprint and master plan for

transforming Africa into the global powerhouse of the future.

It is the

concrete manifestation of how the continent intends to achieve this goal within

a 50-year period. President Ruto is realising and living the dream in this

lifetime.

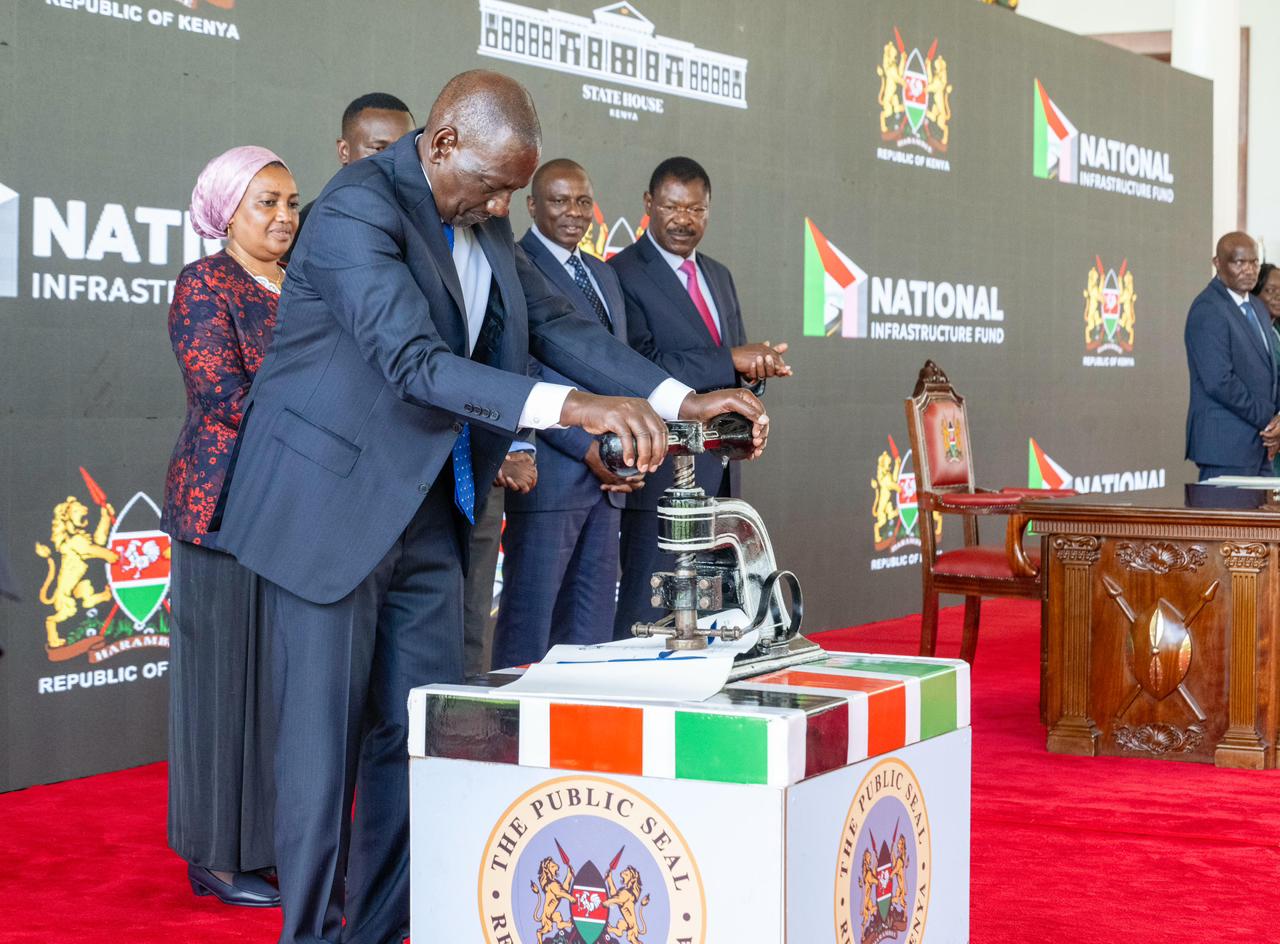

President Ruto using a desk seal press to put an official stamp to the National Infrastructure Fund bill on March 9, 2026 /PCS

President Ruto using a desk seal press to put an official stamp to the National Infrastructure Fund bill on March 9, 2026 /PCS